Synthetix Perps: The First Six Months by Frogs Anonymous

Six months have passed since Synthetix launched the v2 upgrade for their perpetual futures. We’ll do a breakdown of relevant performance statistics below

This report provided by the Frogs Anonymous DeFi Research Team

Introduction

Synthetix is the premier platform for synthetic derivatives on-chain, providing “a liquidity layer that powers an array of on-chain derivatives and financial instruments.” Users stake SNX in a massive, unified collateral pool, and synthetic derivatives are minted against it. A variety of protocols have now integrated with the platform, and they’ve introduced a growing number of assets and instruments that use its liquidity. Today, users can engage with Synthetix to do anything from simple swaps for synthetic ETH to trading leveraged futures on synthetic FLOW.

With this system for amassing liquidity and minting derivatives in place, Synthetix has pursued two goals above all: integrating its liquidity into the backend of the broader DeFi system and building out a suite of products for users to interact with its synthetic assets directly. Kwenta is a perpetual futures exchange, Polynomial offers automated derivatives strategies, and Lyra is a decentralized marketplace for trading options. All of these are built on top of Synthetix’s liquidity, and using Synthetix’s assets. Today we’ll be looking at Synthetix’s perpetual futures, and specifically at performance since their December upgrade to Perps v2.

Synthetix Perps V2

Six months have passed since Synthetix launched the v2 upgrade for their perpetual futures. We’ll do a breakdown of relevant performance statistics below, but first a recap of the changes that Synthetix Perps v2 introduced:

Lower fees by transitioning to off-chain oracles. Historically, Synthetix Perps have relied on on-chain oracles, making trades public upon initiation and enabling front runners to prey on users. In the past, the platform’s response was to raise fees to the point that they were cost-prohibitive to front-runners, but this was obviously not ideal for traders.

As part of Perps v2, the platform has transitioned to off-chain pricing with on-chain validity verification through the Pyth Network. In other words, the price for a trade is pulled off-chain based on a timestamped initiation, then later confirmed on-chain at execution. Without the need to thwart front runners through cost-prohibitive pricing, fees have fallen dramatically to the point that Synthetix perps are among the most competitively priced in the DeFi space. Rather than charging 30-40 basis points for a trade, fees for major pairs (ETH and BTC) are now as low as 0.02% for makers and 0.06% for takers - comparable to most centralized exchanges.

Dynamic Funding Rates. Funding rates are a necessary feature of perpetual futures exchanges, as they prevent the price of futures from drifting too far from spot prices. When the market is skewed long or short, traditional funding rates are paid by one side and received by the other. In this way, futures prices are encouraged to return to delta neutrality.

In the case of Synthetix’s perps, this imperative to maintain delta neutrality is even more important. At any time when market skew is non-neutral, the collateral pool will serve as counterparty to trades, and SNX stakers will essentially be taking the opposite position.

Perps v2 mitigated this risk with the introduction of dynamic funding rates, which are designed to restore delta neutrality more quickly than traditional funding rates. In addition to market skew, the calculation of dynamic funding rates also incorporates velocity. Under this system, the longer the market is skewed in one direction or the other, the more funding rates will get progressively higher, increasing hourly until balance is restored.

For one thing, this affects the trades people may decide to take, as they obviously must factor in the cost of funding rates into their decision making. For another, it encourages arbitrageurs to step in and actively restore balance. This can take the form of funding rate arbitrage or cash & carry trades - either is a viable strategy for arbitrageurs to take, and both play a role in driving price back into a range at which stakers won’t have to act as counterparty.

Introduction of a price impact function based on market skew.

Much like dynamic funding rates, this serves as a risk management tool for SNX stakers. This feature introduces a premium or discount to the price of a futures contract itself, to incentivize users to make trades that contribute to neutralizing market skew. In the same way that influencing the funding rate incentivizes arbitrageurs to affect price, the premium/discount simply accomplishes it through different means.

Trading incentives on Optimism. Synthetix was issued a distribution of early OP tokens upon launch, which were recently delegated to a trading incentives program for perps users. Beginning on April 19th, 300,000 the protocol began distributing 300,000 OP to traders per week, to last for 17 weeks. This is in addition to incentives already being provided by integrators - both Kwenta and Polynomial have rewards of their own, on top of the OP provided by Synthetix.

Data Analysis

Basic stats

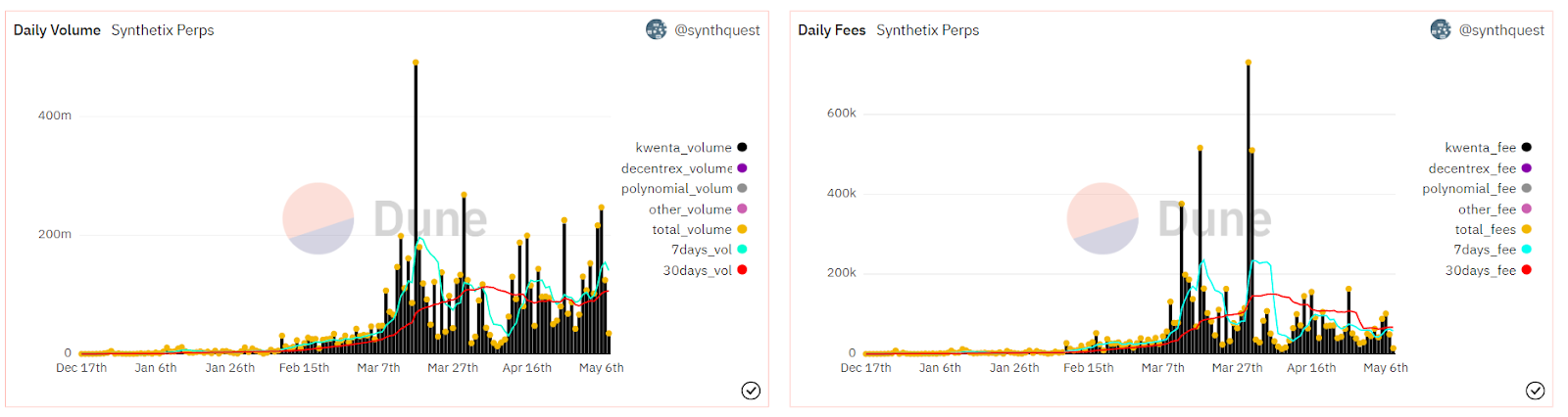

- Volume: $7.18B in volume to date

- $1B in volume in its first 80 days, and another $1B per week 3/10 and 3/17

- Fees: $7.27M in fees to date

- Average daily volume: $53.07M

- Average daily fees: $52,637.18

Looking at the basic volume and fee statistics, Synthetix Perps began to hit its stride in February of this year, going on to generate considerable interest in the middle of March. The most noticeable change in any of these charts - daily volume, daily fees, cumulative volume, cumulative fees, major spikes in volume/fees for sETH and sBTC, uptick in cumulative PnL – all occurred after 3/16, the day CPI numbers were released and BTC ostensibly decoupled from the equities market after a number of banking collapses. Judging by the moving averages on the daily volume chart, this surge of interest has been sustained ever since, with volume plateauing a few weeks later and remaining generally constant ever since.

Exchange Breakdown

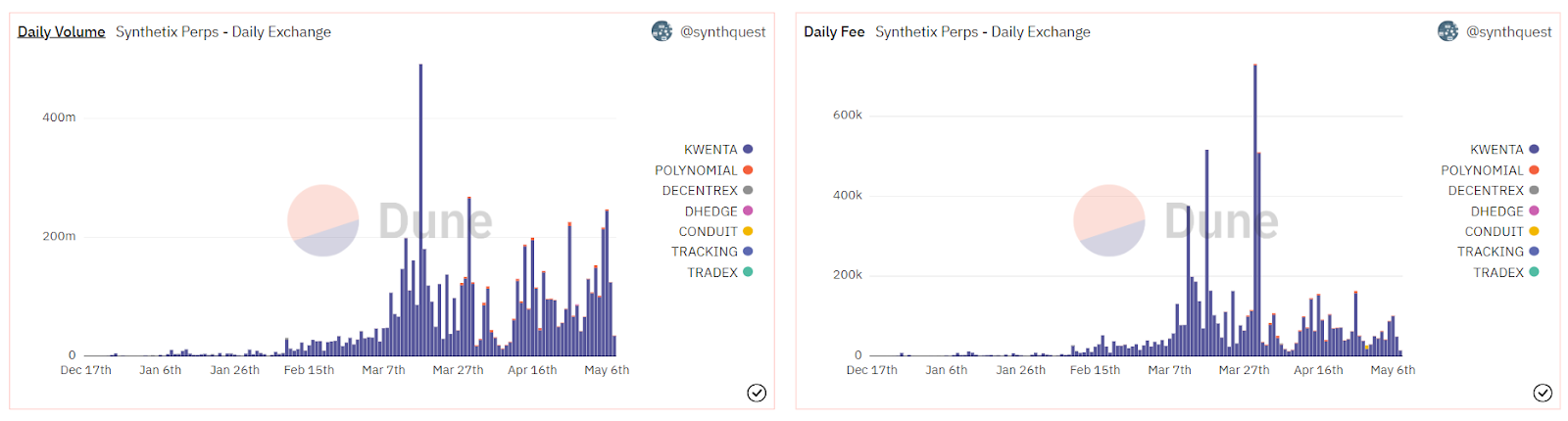

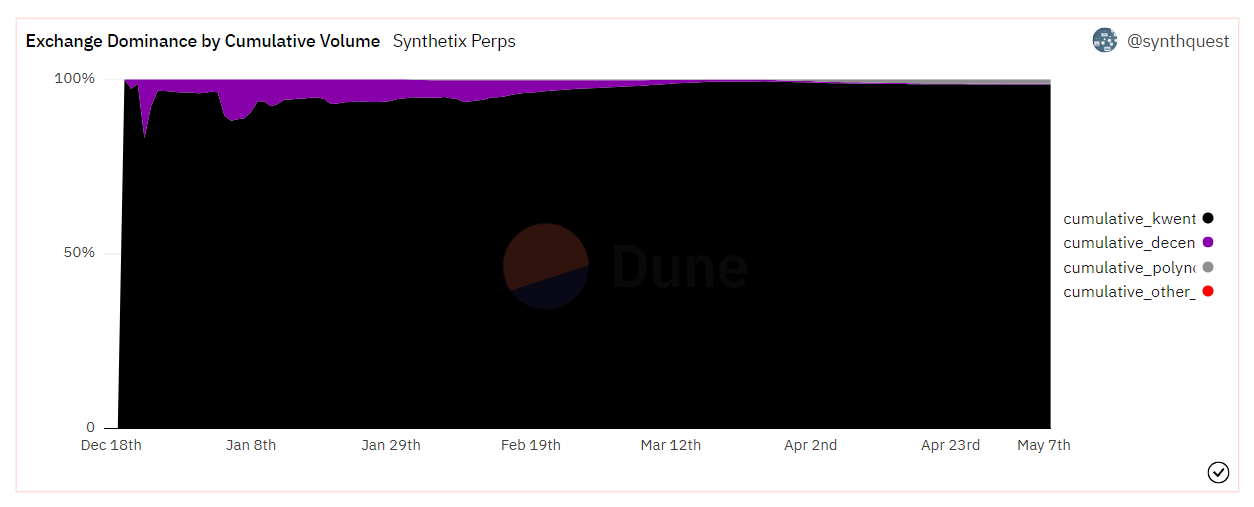

Looking at the exchange dominance chart, trading volume on Synthetix Perps is overwhelmingly driven by Kwenta, Synthetix’s flagship perps platform. Kwenta currently accounts for 98.6% of cumulative trading volume, with Polynomial and Decentrex falling in a distant second and third place.

While Decentrex once peaked at 16.8% of trading volume, its numbers have dwindled to almost zero, and we can see its cumulative dominance trail off as Kwenta and other competitors continue to see brisk trading. Polynomial, on the other hand, has grown rapidly over the past month, overtaking Decentrex by dominance towards the end of March and now accounting for 1.2% of total perps trading volume.

Looking into this a bit, it may not be a coincidence - on March 27th, Polynomial launched Polynomial Trade, a significant upgrade that brought deeper liquidity, reduced fees to 5-10bps, and introduced limit orders to the platform. Clearly this has resulted in a dramatic uptick in usage, as we can see in the charts above.

For now, though, Kwenta still reigns supreme, in part due to its generous token rewards program. This lead logically extends to fees as well. With $7.26M in revenue, it accounts for 98.5% of cumulative fees on Synthetix Perps, with Polynomial far behind at $78,541.

Asset Breakdown

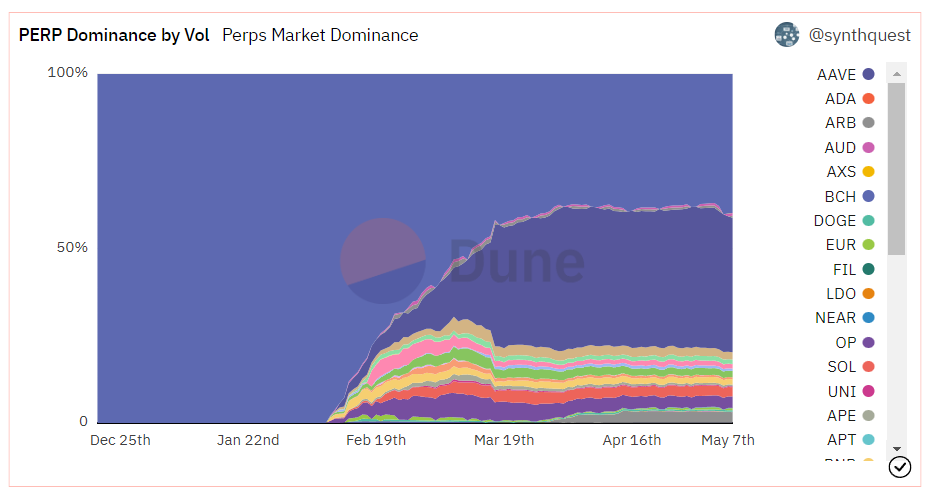

Moving on, we can examine the dominance of particular perps to get a sense of which assets are being traded most heavily on the Synthetix platform. Predictably, volume is dominated by sBTC and SETH, with noticeable spikes in these assets on volatile trading days.

At 40% of trading volume, sETH in particular has a sizable lead. Its dominance has been trending down since other assets were introduced on 2/8, though it seems to have stabilized around this level over the past two months. Similarly, sBTC has expanded continuously since its debut, with growth moving largely in lockstep with BTC.d in the spot market.

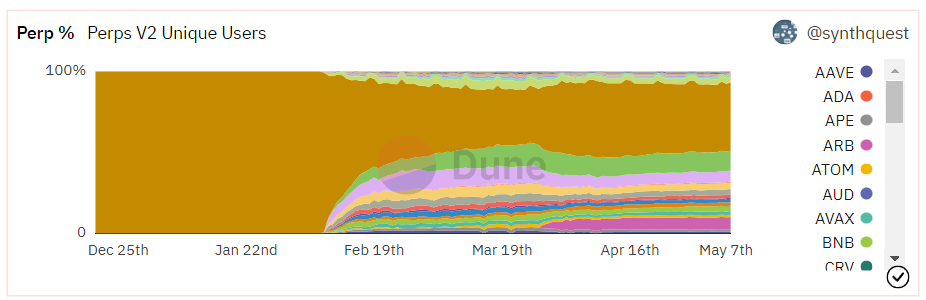

One interesting observation can be made by comparing the chart for perp dominance with the chart for percentage of unique users: sBTC represents 38.5% of the Synthetix Perps volume, but is only being used by 12.3% of users. This suggests that a small number of larger accounts are disproportionately trading BTC at the moment, potentially to hedge growing spot positions.

On the other side of the aisle, we see that 7.4% of users are trading ARB while it only accounts for 3.0% of daily volume. Given ARB’s popularity and visibility on crypto Twitter, and considering recent activity in the BTC market (As per Glass Node, wallets with 10,000+ BTC have been accumulating while everyone else distributes), we may be able to deduce that BTC perps are being used to hedge massive spot positions while ARB perps are being used by small accounts to speculate on price movement. Only one theory, but it illustrates how perps data can provide valuable information for users trying to determine whether or not to accumulate, distribute, or hedge their existing positions. The data is definitely worth paying attention to.

Comparison to similar protocols

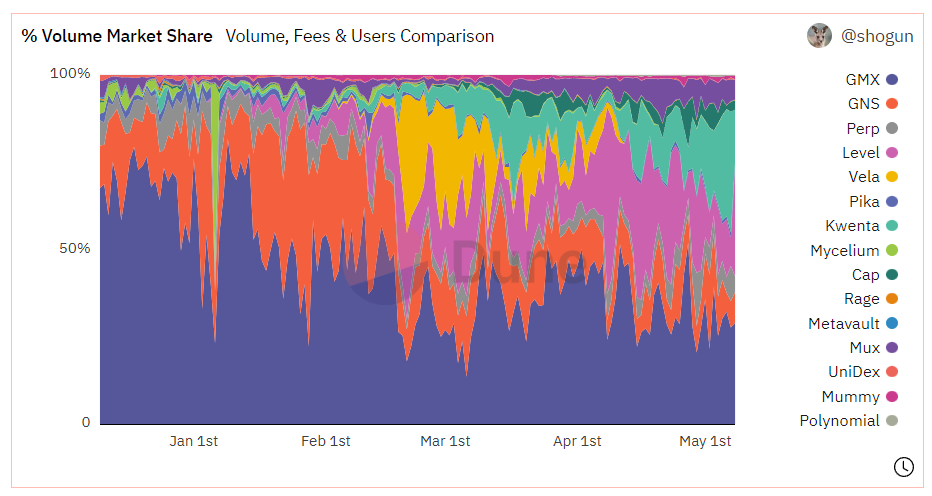

Moving on to examine the relative dominance of different perps platforms, we can essentially use Kwenta as a stand-in for Synthetix Perps, as it accounts for over 98% of platform volume. With this in mind, Kwenta has grown continually since the launch, reaching 28.6% market dominance during the March 17th event discussed above. The platform has only continued its expansion, though, peaking at 34.5% of market share by volume, temporarily overtaking GMX - quite an accomplishment.

For obvious reasons, there is considerable volatility in activity and the numbers vary dramatically from day to day. At this peak however (yesterday), the platform had:

- 34.5% of volume from all decentralized perps platforms

- 14.0% of all fees

- $124.06M in daily volume

One observation we can make from these charts, however, is the discrepancy between market share by volume vs. fees. While Kwenta was briefly the leading perps platform in all of DeFi on 5/7, its 34.5% in market dominance dramatically overshadowed its 14.0% dominance as measured in platform fees. While higher protocol revenue would be nice, we can draw a sunny conclusion from this nonetheless - the explosion in volume and subsequent expansion in market dominance is likely a product of the low fees. As users are drawn to a more cost effective product, market share by volume will likely increase exactly as market share by fees goes down - and fee revenue in absolute terms will inevitably rise.

The Future of Synthetix Perps

Already in a state of marked growth, Synthetix has a number of plans for Perps that will likely contribute to its expansion. SIP-298 has recently been approved and implemented, which introduced nine new perpetuals markets on Synthetix Perps: APT, LDO, ADA, GMX, FIL, LTC, BCH, SHIB, and CRV. With these online, SIP-2014 and SIP-2015 are also being considered, which will include PEPE, SUI, and BLUR, and XRP, DOT, TRX, FLOKI, and INJ, respectively. Finally, SIP-2009, currently being in draft, also proposes to introduce a perpetual contract for the ETH/BTC ratio, which would truly usher in a new era of trading on a platform that - as we’ve seen - is dominated by large wallets hedging their exposure to ETH and BTC.

Ultimately, we can gain a tremendous amount of insight from looking at the perps data in this way, and the conclusions are valuable: we see that Synthetix Perps is a platform in a state of dramatic growth, and that volume has expanded in tandem with reduced fees - a clear sign that the upgrade is paying off. We can also learn a lot about the market itself - namely, observing the behavior of large wallets can inform our interpretation about general market sentiment. Finally, we can chart Synthetix Perps steady takeover of the perpetual futures market in DeFi, see that the platform reached its highest all-time volume only yesterday, and conclude that its growth is active and robust. Clearly the best days have only just begun.